Your retirement simulator says you hold 60% stocks and 40% bonds. It generates random returns for each, independently, thousands of times. The problem? In 2008, stocks dropped 37%. A truly independent bond draw might show bonds dropping too - or rallying - with equal probability. But in reality, government bonds rallied 5% that year. The independence assumption throws away the single most important reason you diversified in the first place.

This is why correlation modeling matters. And why most basic Monte Carlo calculators get it wrong.

The Independence Problem

A Monte Carlo retirement model generates thousands of return sequences to stress-test your plan. If it treats each asset class as a separate coin flip, it produces scenarios that are statistically possible but economically nonsensical.

Some simulated years might show stocks crashing 30% while bonds also crash 20%. Others might show stocks booming while bonds boom equally. Both can happen, but they happen far less often than an independent model suggests. The correlation between stocks and bonds has historically been slightly negative (around -0.1 to +0.3), meaning bonds tend to hold value or rise when stocks fall.

When you ignore this, two things go wrong:

Diversification benefits disappear. The whole point of a 60/40 portfolio is that bonds cushion stock crashes. An independent model does not capture this cushion. It treats your diversified portfolio as if you just randomly hold two unrelated bets.

Portfolio-level volatility is wrong. A 60/40 portfolio with stocks at 16% volatility and bonds at 6% does not have 12% blended volatility (the weighted average). Because of negative correlation, the actual portfolio volatility is closer to 10%. Getting this wrong means your variance drain estimate is off, your percentile bands are too wide, and your success rate is unreliable.

How Cholesky Decomposition Fixes This

Cholesky decomposition is the standard technique for generating correlated random variables from independent ones. The idea is straightforward even if the name sounds intimidating.

-

Start with independent random draws. The simulator generates three random returns - one for stocks, one for bonds, one for cash - each drawn independently from their respective distributions.

-

Define how assets relate. A correlation matrix specifies how each pair of assets co-moves. Stocks and bonds might have a correlation of -0.10. Stocks and cash might be near zero. This matrix encodes the structure of your portfolio's risk.

-

Transform the draws. Cholesky decomposition factors the correlation matrix into a lower-triangular matrix. Multiplying the independent draws by this matrix produces correlated returns that respect the relationships you specified.

The result: when the simulator draws a bad year for stocks, it is more likely to draw a flat or positive year for bonds. When it draws a boom for stocks, bonds might underperform slightly. The simulated scenarios look like actual multi-asset market behavior, not random noise.

Crisis Correlations: When Diversification Fails

Here is where it gets more complicated. The correlation between stocks and bonds is not constant. It shifts with market conditions.

During normal times, stocks and bonds have low or slightly negative correlation. This is the regime where diversification works as advertised. But during certain crises, correlations can spike. In 2022, both stocks and bonds fell significantly as interest rates rose. The 60/40 portfolio - supposedly the conservative choice - lost roughly 16%.

This phenomenon is called correlation breakdown (or more precisely, regime-dependent correlation). The diversification benefit you counted on shrinks exactly when you need it most.

A fixed correlation matrix handles normal conditions well, but it cannot capture these regime shifts. Some advanced approaches use separate correlation matrices for different market environments (calm vs. stressed), but even a fixed matrix with realistic values is a massive improvement over independent draws.

For retirement planning, the practical implication is clear: do not assume that your stock-bond diversification will always provide the same cushion. Stress-test your plan with higher correlations (say 0.3-0.5 instead of -0.1) to see what happens when the cushion deflates.

Why This Matters More Under Fat Tails

Correlation modeling interacts with fat-tail distributions in an important way. Fat tails produce more extreme returns. If those extreme returns are generated independently across asset classes, you get an unrealistic picture: your portfolio occasionally experiences simultaneous crashes across all assets at frequencies that do not match reality, while also occasionally experiencing simultaneous booms that are equally unlikely.

With Cholesky-correlated returns under fat tails, the extreme scenarios become more realistic. A stock crash is paired with a plausible bond response. A bond sell-off is paired with a plausible stock reaction. The tail events are still extreme - fat tails guarantee that - but they are extreme in ways that actually happen.

This is especially important for sequence-of-returns risk. The damage from a crash in year 1-3 of retirement depends not just on how far stocks fall, but on whether bonds provided a cushion. A crash where bonds also fall (correlated stress) is far more damaging than one where bonds rally (negative correlation working as intended). Only a correlated model can tell you the difference.

What About Three or More Assets?

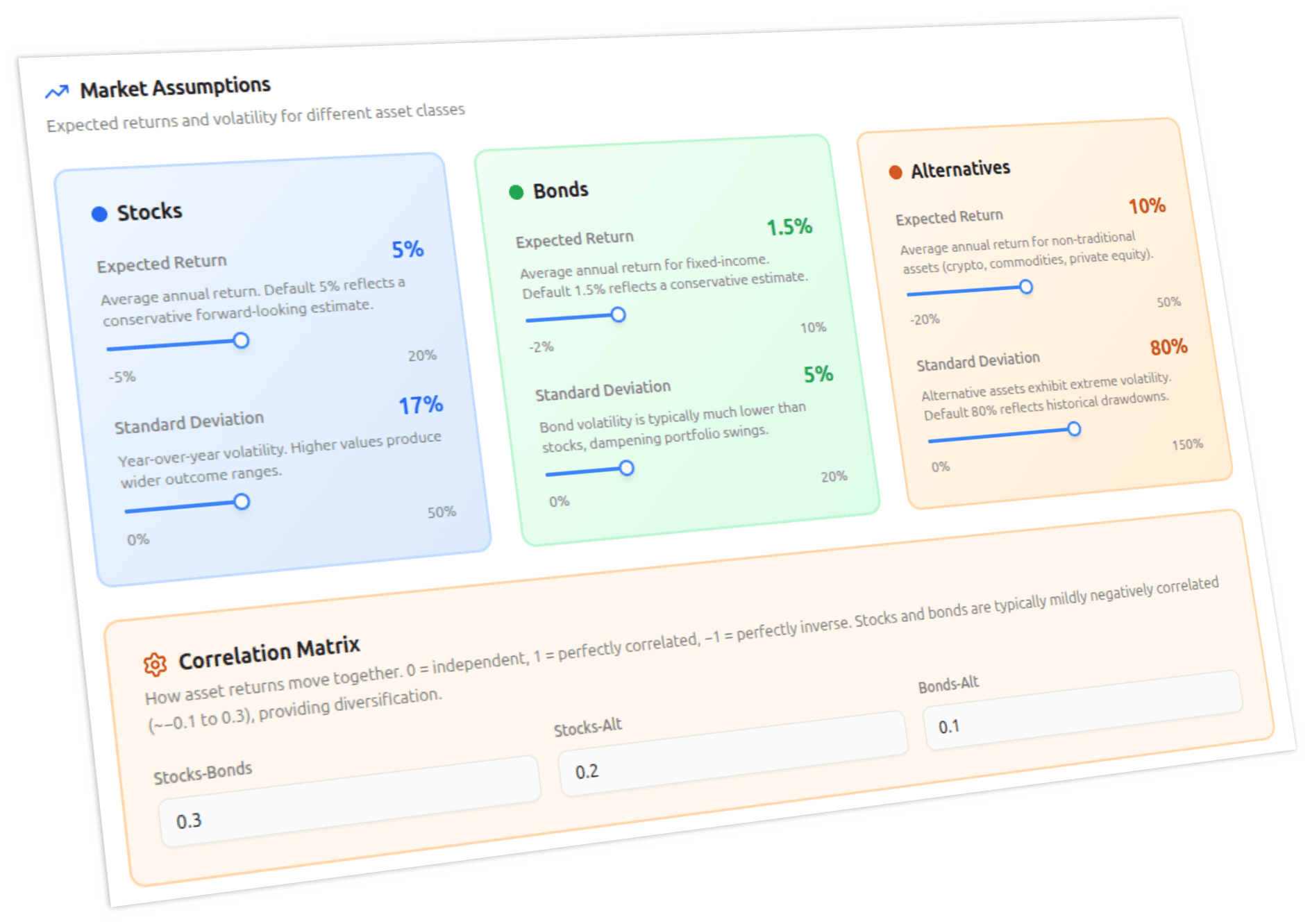

Most retirement portfolios involve at least three asset classes: stocks, bonds, and cash (or alternatives). The correlation matrix scales to any number of assets, but the relationships become more complex.

For a 3-asset portfolio, you have three pairwise correlations to specify:

| Stocks | Bonds | Cash | |

|---|---|---|---|

| Stocks | 1.00 | -0.10 | 0.05 |

| Bonds | -0.10 | 1.00 | 0.15 |

| Cash | 0.05 | 0.15 | 1.00 |

The diagonal is always 1 (every asset is perfectly correlated with itself). The off-diagonal values capture the pairwise relationships. Cash has near-zero correlation with both stocks and bonds, making it a genuine diversifier - but with low expected returns, it reduces portfolio growth.

The Cholesky decomposition handles any positive-definite correlation matrix, so scaling from 2 to 3 assets is a mathematical non-issue. The hard part is choosing realistic correlation values. Historical data gives you a starting point, but correlations shift over decades. Using a range of assumptions - conservative, moderate, and stressed - gives you a more honest picture than any single set of values.

Independent vs Correlated: How Much Does It Matter?

The impact depends on your portfolio's allocation and the market environment you are stress-testing:

For a 60/40 stock/bond portfolio: switching from independent to negatively correlated returns typically improves the median outcome and narrows the percentile bands. Your success rate might rise by 2-4 percentage points because the model correctly captures the bond cushion.

For an all-equity portfolio: correlation modeling matters less, because there is only one risky asset. The main benefit comes if you split equities into domestic and international with their own correlation structure.

Under crisis conditions: the difference is most pronounced. Independent models might show a 5th percentile outcome of portfolio depletion at age 78. A correlated model with realistic crisis behavior might show depletion at 75 (because the bond cushion is smaller than the independent model assumed) or at 82 (because the bond rally was captured). The direction depends on the correlation values.

The key insight: independent models are not just imprecise. They are wrong in different directions depending on the scenario. Sometimes they are too optimistic, sometimes too pessimistic. You cannot even tell which way the error runs without modeling the correlations explicitly.

What This Means for Your Plan

Do not trust a simulator that treats assets independently. If your Monte Carlo tool does not mention correlation or Cholesky decomposition, it is generating unrealistic multi-asset scenarios. The results might look reasonable in aggregate, but the individual scenario paths are wrong.

Test with different correlation assumptions. Historical averages are a reasonable baseline, but run your plan with stressed correlations (higher positive values) to see what happens when diversification partially fails. If your plan only works under favorable correlations, it is more fragile than the headline success rate suggests.

Correlation does not replace fat-tail modeling. They address different problems. Fat tails fix the frequency of extreme events. Correlation fixes how assets interact during those events. You need both for a realistic picture.